Related Articles

The most visible bitcoin buyers in the world are buying at near-record pace. It is not enough.

In a weekly report by CryptoQuant that showed overall 30-day apparent demand at 63,000 $BTC as of late March, the market is selling much faster than institutions can absorb. During the 30-day window that is rolling, ETF purchases were at about 50,000 $BTC (the highest since October 2025) and hit around 500,000 $CTC. It was accumulating strategy that stood steady at about 44,000 $BTC. In March about 94,000 $BTC was absorbed by the two largest institutional channels, together under one of these namesake institutions as well.

The rest of the market retail, older whales, miners, funds – sold about 157,000 $BTC in the same period if institutions bought 94,000 $BCTC and net demand is still negative 63,000.

At least four other independent indicators are pointing in the same direction.

The whale reversal

The market’s largest buyers have become large holders, wallets of 1,000 to 10,000 $BTC, which has been transformed into its biggest sellers on a scale CryptoQuant describes as one of the most aggressive distribution cycles ever recorded.

A year ago, these wallets were collectively putting 200,000 bitcoin in their holdings of the currency. Today they are collectively removing 188,000 from . That’s a roughly 400,000 $BTC swing from accumulation to distribution in about 18 months, according to .

Wallets of $100 to 1,000 $BTC, mid-tier holders are still technically stacking but the pace has been more than 60% since October 2025 from nearly 1 million $ BTC in annual addition and 429,000. They haven’t stopped buying . But they’ve dramatically slowed down, s.

The realized price compression

At its $67,000-$68000 range, Bitcoin’s spot price is 21% above its real cost of $54,286, the mean value for every coin on network weighted by its final transaction. coinded in the week, CoinDesk noted that “the average holder is still profitable (which historically means market has not bottomed) that’s what it does to be true.

A signal marked the true cycle low was spot falling below realized price in 2022, a sign that fell below real cost. Bitcoin sprang up on its aggregate cost basis from June through October of that year, and the deepest point (about 15% below realized) coincided almost exactly with the low near $15,500.

It’s not the current setup of . And that gap is slaming fast,’ says. The premium to realized price was around 120% when bitcoin went up $119,000 in late 2024. One of the quickest approaches to the real price line outside of outright crashes is that That has compressed to 21% in about 15 months, one of those fastest ways to prevent an actual price range.

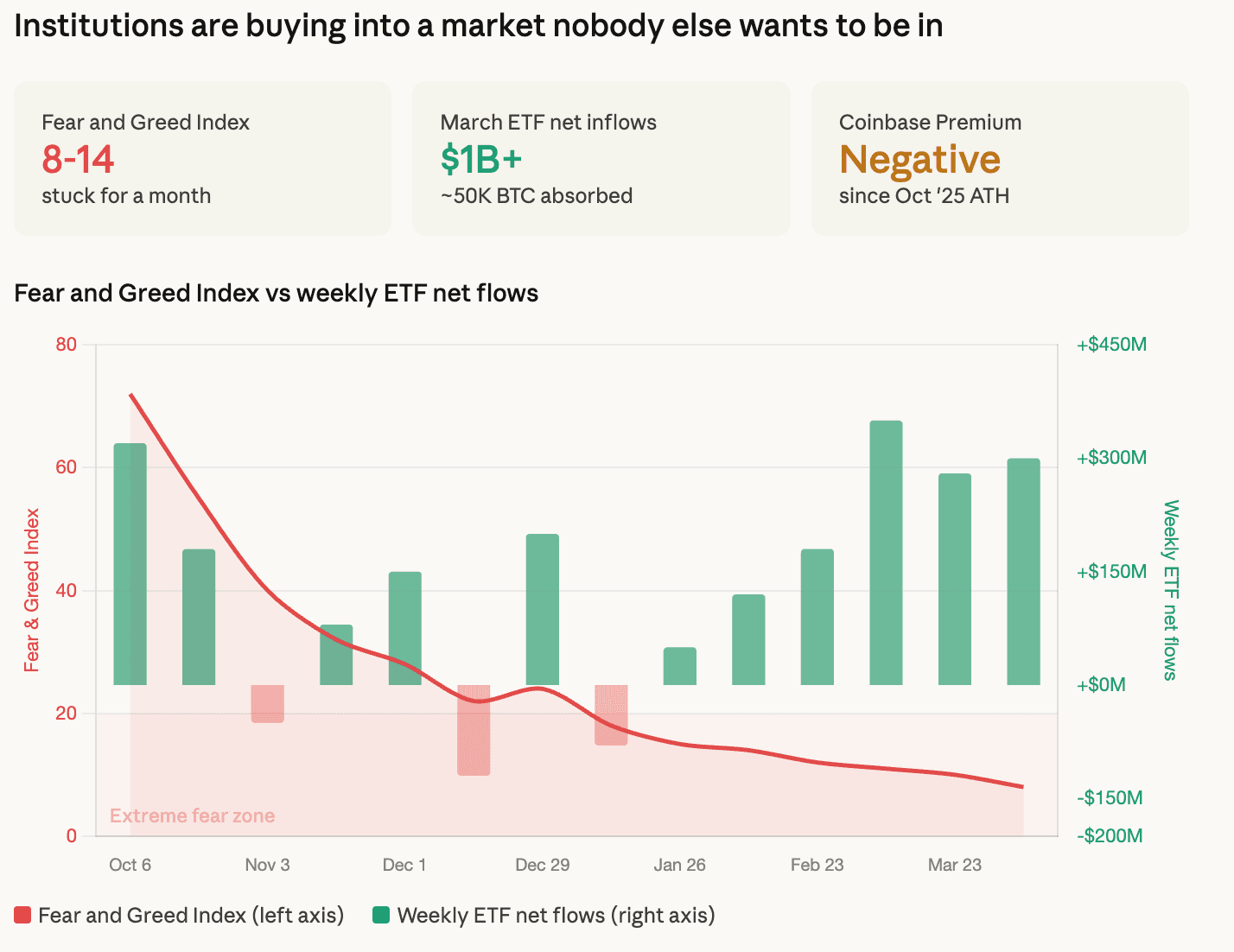

The sentiment disconnect

deep into the extreme fear territory of last month, has been stuck between 8 and 14 for the past month as a result of The Fear and Greed Index. But in March, over $1 billion was flown in net to attract more than one billion inflows from yet bitcoin ETFs.

That combination of extreme fear and strong institutional buying is unusual, . The flows are not resulting in greater confidence, it means that the flows do not translate to an overall confidence; institutions are buying into a market which the rest of the participants would be interested in.

The popularity of the popular Coinbase Premium Index bolsters this assertion. metric, which measures whether bitcoin is trading at a premium or discount on Coinbase relative to other exchanges and acts as ‘proxy for U.S.” s S Since bitcoin’s all-time high above $126,000 in early October 2025, institutional appetite has been persistently negative since its historic high over $16,000. Americans have not returned to the scale of s even with prices in the $65,000-$70,000 range.

The war pattern

This is a behavioral explanation for the demand drain, which can be seen in the price action of the last five weeks. Bitcoin, which has smashed the entire Iran conflict from $65,000 to $73,000, sold on every escalation headline, rallied all de-emphalling headline and ended up roughly where it started. Trump’s address promised to hit Iran “extremely hard,” and Monday’ 4% equity rally on ceasefire optimism returned by Wednesday, after the country lost its ability to achieve an end-to-day promise of hitting Iran. He said ‘Although s are in the line, “

The pattern of hope, headline, reversal repeats with such regularity that the dominant strategy has become not to be at all in position. That is shown in the demand data as a gradual withdrawal rather than panic selling, and that appears instead of “that” (short-term ) on this list.

The drawdown is compressing, not ending

This drawdown from October’s all-time high above $126,000 is about 47%, much less serious than the 84% to 87 per cent crashes that followed the 2013 and 2017 peaks. In late March, Fidelity Digital Assets analyst Zack Wainwright noted that bitcoin’s growth is “less impulsive,” with the risk of extreme downside events lessened as the asset matures.

But Jason Fernandes, co-founder and market analyst at AdLunam said ‘Bitcoin’t drawdowns that are about half the size of a mature market structure is. In addition to institutional participation, volatility naturally compresses on both the upside and the downside as liquidity deepens,” a statement that suggests “As long as we have been in liquidity for many years”, which is also known as an example of how volatile it has become.

Demand data is dependent on the framing of drawdown compression for the demand data. If bitcoin is maturing into an asset where 50% corrections replace 85% crashes, then the current contraction may not be resolved with the violent capitulation flush that marked previous cycle bottoms.

What could change this

Two catalysts sit on the near-term horizon.

The approval of this week for a bitcoin ETF charging just 14 basis points, 11 below the category average, was given to Morgan Stanley. It also allows 16,000 financial advisors to work with $6, a product that is open to . This is a channel that has not previously exposed bitcoin ETF directly and it’s 2 trillion, which was the first channel to have been subjected to direct bitcoin.

Strategy’s STRC preferred equity product received hundreds of millions inflows around its recent ex-dividend date, which is the funding mechanism for 44,000 $BTC per month accumulation. If that repeats and accelerates every month, it adds another layer of sustained buying pressure to the .

However, it would remain a single company running a leveraged bitcoin strategy.

In a short-term rebound, according to the report by CryptoQuant, could be $11,500–81,000200 as long as the Iran conflict de-escalates, which corresponds with the Lower Band and Trader On-chain Realized Price resistance zones.

These two metrics measure the average cost basis of short-term and active traders respectively, which have historically served as ceilings during bear market rallies. Bitcoin is currently trading below both of these two currencies.

The read across all five data sources is that bitcoin’s demand structure is thinning from the inside.

That doesn’t mean the current floor of range, but that it is entirely dependent on whether ETFs, Strategy and the new Morgan Stanley channel can still absorb what the rest of the market is trying to sell off.

Thanks for reading Five data sources say the same thing about bitcoin market Its thinning from the inside